Latest Update:

Growth Manager

Most founders walk into their first meeting with a VC trying to close the deal. That's the wrong goal entirely, and it's the reason so many first VC meetings don't lead to a second one.

A typical VC sees around 1,000 companies a year, meets with roughly 200, and invests in about 4. Your job in that first meeting isn't to be one of the 4. It's to be one of the handful who gets called back. Everything else flows from that.

This guide covers exactly what VCs are scanning for in a first meeting, how to structure your time, the preparation moves that separate serious founders from everyone else, and how to run the conversation so you leave with momentum, not a polite "we'll be in touch."

Quick Takeaways

The primary goal of your first meeting with a VC is to earn a second meeting, not to close the round.

VCs make gut-level decisions fast; clarity and specificity matter more than comprehensiveness.

Cover five areas: Team, Problem, Solution, Market, and Traction (in that priority order if you get cut short).

Send a non-confidential deck 2–3 days in advance so the VC comes prepared with sharper questions.

Ask smart questions back. A good first meeting is a two-sided conversation, not a one-way pitch.

Follow up within 24 hours with a short note and any data the VC requested.

Who you're meeting (associate vs. general partner) changes your tactical approach.

What Is the Goal of Your First VC Meeting?

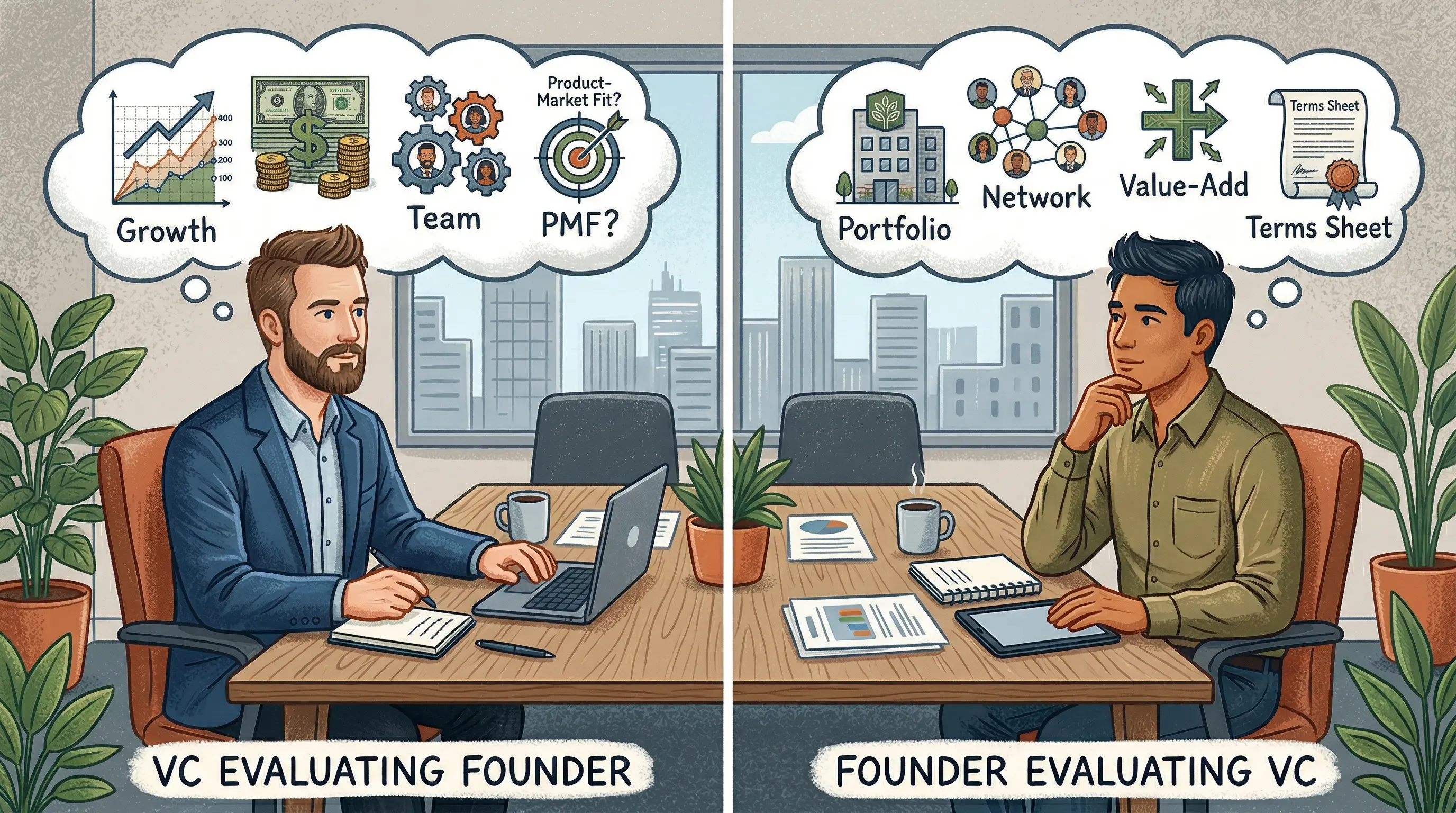

The goal of your first meeting with a VC is to get a second meeting. Not to get a term sheet. Not to close the round. The first meeting is a compatibility screen, not a due diligence session. Your job is to be interesting enough, credible enough, and easy enough to work with that the VC wants to go deeper. Everything you do in that room should serve that single objective.

This sounds obvious. But most founders go in pitching like it's their last shot, cramming in financials, product roadmaps, and competitive breakdowns that belong in meeting three. The result is a dense, one-directional presentation that gives the VC nothing to ask about and no reason to follow up.

The best first meetings feel like a conversation between two people figuring out if they have something in common. One person talks more. That's fine. But it's still a dialogue.

How Long Is a First VC Meeting and How Should You Structure It?

First meetings come in two formats, and your approach should shift depending on which one you're in.

The Standard 30-Minute Call

This is the most common format for initial outreach, especially with larger firms where partners have packed schedules. Thirty minutes goes fast. Here's how to use it:

Minutes 0–5: Quick introductions. Who you are, why you're building this, and one sentence on what the company does.

Minutes 5–15: Your pitch. Lead with your strongest signal immediately: massive traction, unique founder-market fit, or a market insight the VC hasn't heard before. Don't bury the lead.

Minutes 15–25: Investor Q&A. This is where VCs test depth. Be ready for interruptions; they're a good sign, not a disruption.

Minutes 25–30: Next steps. Ask about their process, timeline, and what they'd need to see to move forward.

In 30 minutes, you have time to make one strong impression. Pick your sharpest point and make sure you get to it early.

The 60-Minute Meeting

A longer first meeting usually means the VC has already reviewed your deck and wants to go deeper. Use the extra time this way:

Minutes 0–10: Introductions and context-setting. This is also where you can ask the VC about their recent investments or current thesis to calibrate the conversation.

Minutes 10–25: Your pitch, with room for more depth on the problem and traction.

Minutes 25–45: Real dialogue. By now, a good VC will be pushing back, asking pointed questions, and stress-testing your assumptions. Lean into it.

Minutes 45–55: Questions you ask them.

Minutes 55–60: Agree on clear next steps.

In a 60-minute meeting, you have time to let the conversation breathe. Don't fill every minute with slides.

What VCs Are Actually Looking For in a First Meeting With a VC

VCs make initial decisions in under two minutes. They're running a mental checklist while you talk, and it maps to five areas. Know these before you walk in.

1. Team

This is the first filter, especially at pre-seed and seed. Investors are betting on people before they're betting on products. They want to know why you and your team are the right people to solve this specific problem.

A strong answer doesn't just list credentials. It explains the connection between your background and the problem. If you spent six years in hospital operations before building a healthcare scheduling tool, say that explicitly. If you and your co-founder have shipped something together before, mention it. VCs are skeptical of founding teams that have never worked through hard problems together.

What doesn't land: a list of impressive-sounding jobs with no through-line to what you're building.

2. Problem

VCs want to know the pain is real, expensive, and not going away on its own. The strongest founders show obsession with the problem, not just the solution. That means customer research, specific stories from users, and data on how much the problem costs the people experiencing it.

"We talked to 80 restaurant owners about food waste before writing a line of code" is more convincing than "there's a $12 billion market in food waste."

3. Solution

Here's something most first-time founders don't realize: VCs at the early stage are not judging your current product. They're judging your product vision and your ability to think through a path from here to there.

If your MVP is rough, don't apologize for it. Describe what you're building toward, the milestones on the way, and what you'll have learned in the next six months. Early-stage investors know the product will change. They're investing in your judgment about how it should change.

4. Market

VCs need to believe there's a big enough market to justify a venture return. "Big enough" usually means a potential outcome in the hundreds of millions or billions, because most of their portfolio won't return capital and the winners have to carry the fund.

The strongest market pitches don't just cite a large TAM number. They show a reasoned argument for why the market is growing, why now is the right time to enter it, and what the wedge is: the initial segment where you can win before expanding.

5. Traction

Traction is whatever proof you have that the world wants what you're building. At pre-seed, that might be letters of intent, waitlist signups, or early customer conversations. At seed, VCs expect at least some revenue data, retention numbers, or contracted pilots.

Whatever you have, show numbers that actually connect to business fundamentals. Month-over-month growth in active users matters. Total app downloads usually doesn't.

Pro Tip: Don't lead with traction if your numbers are thin. Lead with team and problem instead. Traction will come up in Q&A regardless, and you're better off setting a strong qualitative foundation first.

How to Prepare Before the Meeting

Most founders underprepare. A few overprepare in the wrong direction, memorizing a script instead of knowing their business cold. Here's what actually moves the needle.

Send Your Deck 2–3 Days in Advance

This is one of the best moves you can make before a first meeting with a VC. When a VC reviews your deck in advance, they show up with sharper, more specific questions instead of surface-level ones. The conversation starts deeper and covers more ground.

Keep the deck you send in advance non-confidential. Detailed financials, proprietary data, and customer lists can come later. The pre-meeting deck should prime the VC to understand what makes your startup unique, not overwhelm them with information they can't process in 15 minutes.

Make it forwardable. If the VC can pass it to a colleague who might be a better fit, you've just expanded your reach without any additional effort.

Know Your Numbers Cold

You don't need a complete financial model for a first meeting. You do need to know your key metrics without hesitating. Customer acquisition cost, lifetime value, burn rate, runway, month-over-month growth rate. If you stumble on any of these, it signals that you're not close enough to your business.

Practice saying these numbers out loud before the meeting. Not reading them from slides. Saying them naturally, the way you'd tell a friend.

Research the Firm and the Person You're Meeting

This is table stakes, but most founders don't do it well enough. Read the firm's investment thesis. Look at their last 10 investments. Know which partners focus on what. And find out exactly who you're meeting.

This last point matters more than most guides acknowledge: who you're meeting at a VC firm changes how you should run the conversation.

If you're meeting an associate or principal, they're typically screening for whether the opportunity is worth a partner's time. Be clear and compelling on the basics. Don't assume they have authority to move the deal forward alone. Ask them directly what the next step looks like and who else gets involved in the decision.

If you're in the room with a general partner or managing director, the bar shifts. They're asking themselves whether they can work with you for the next 7–10 years. That means the relationship dynamic matters as much as the pitch content. Be a person, not a deck.

Your Deck Design Is a Pitch Before You Say a Word

A founder who walks into a first meeting with a polished, well-designed Pitch Deck is communicating something before they've opened their mouth: they understand that presentation matters, they have an eye for quality, and they're serious about fundraising.

A messy, inconsistent deck sends the opposite signal. VCs process information visually, and a deck that looks like it was assembled the night before reflects on your attention to detail as an operator.

If you're raising and your deck looks rough, fixing it before your first meetings is worth the time. The design quality of your fundraising materials shapes the impression you make before the conversation even starts.

How to Run the Meeting Like a Pro

Preparation gets you in the room. How you run the meeting determines whether you leave with a second one.

Open With Your Strongest Card, Not Your Origin Story

Founders are often tempted to open with the story of how they came up with the idea. Save that for later in the meeting or for the second meeting. VCs have short attention spans and are constantly making subconscious triage decisions about whether to stay engaged.

Open with whatever is most compelling about your company right now. Strong early traction, a founder-market fit story that's immediately credible, or a market insight that reframes how the VC thinks about the space. Make them lean in before you tell them your journey.

Answer Questions Directly, Then Expand

This sounds simple. It isn't. Most founders, under pressure, give long, hedged, circular answers that bury the actual response. VCs notice this immediately.

The format that works: give a direct one-sentence answer, then ask if they want more detail. "Yes, we're growing 20% month-over-month for the past four months. Want me to walk through the breakdown?" That's a confident answer. It's also a natural conversation move.

Release the Agenda

The worst thing you can do in a first meeting with a VC is say "I'll get to that on slide 10." The VC just told you what they want to know, and you've told them to wait. You've killed their momentum and confirmed you're more attached to your script than to the actual conversation.

If a VC asks a question, answer it. Rearrange your flow on the spot. The best pitches aren't pitches at all. They're conversations where the founder happens to be very well prepared.

What to Do When You Don't Know the Answer

This happens in every first meeting. A VC asks something you haven't thought through yet, or asks for a number you don't have memorized.

Don't fake it. VCs have pattern-matched thousands of founders and they can tell when someone is hand-waving through an answer. Getting caught in a bluff destroys trust far more than admitting you don't have the answer.

The right move: "That's a good question and I want to give you a real answer, not a guess. Let me pull the exact numbers and send them over today." Then do it. You've just given yourself a reason to follow up with something useful, and you've shown the VC that you're honest under pressure.

How to Extract Value Even When It's Not a Fit

Some first meetings become obvious early: the VC doesn't invest at your stage, or they're already backed a competitor, or the thesis just doesn't align. Most founders either don't notice or keep pitching anyway.

The sharper move: acknowledge it and pivot. "It sounds like we might not be in your sweet spot right now, but I'd love your perspective on [specific question about the market or our approach]." You've released the pressure of the pitch, turned the VC into a collaborator instead of a judge, and created the conditions for them to send you to someone who is a better fit.

VCs know each other well. A warm intro from a VC who passed is often more valuable than a cold approach to the right VC.

Smart Questions to Ask the VC

Asking good questions is one of the fastest ways to signal that you're a serious, thoughtful founder. It also tells you things you need to know before you decide whether this is the right investor for you.

Here are the questions that consistently produce useful information:

"What does your typical decision-making process look like after a first meeting?" This tells you the timeline, who else you'll need to impress, and what materials to prepare.

"What's your average check size and ownership target?" If there's a structural mismatch between what they write and what you need, better to know now.

"How does our company fit into what you're focused on right now?" This forces the VC to articulate the thesis connection, and their answer tells you how seriously they're considering the opportunity.

"How do you typically work with founders after an initial investment?" Some VCs are hands-on operators; others are passive capital. Neither is wrong, but it needs to match what you want.

"Is there anything we didn't cover today that you'd want to understand better before moving forward?" This gives the VC permission to flag gaps, and it tells you exactly what to address in your follow-up.

The underlying principle: you're not just auditioning for their capital. You're deciding whether to take their money and give them a board seat. Act like it.

Common Mistakes That Kill Your First Meeting With a VC

Most first meetings don't fail because of bad businesses. They fail because of avoidable mistakes in how founders show up and run the conversation.

Didn't research the firm. VC firms publish their investment thesis publicly. Showing up without knowing what they invest in (stage, sector, check size) is an immediate signal that you either didn't do the work or you're mass-pinging every VC you can find. Neither is a good look.

Rambling. Investors have short attention spans by design. They're moving between dozens of conversations and constantly making triage decisions. If you go on long tangents or take three minutes to answer a yes-or-no question, you'll lose them. Practice keeping answers short and specific.

Clinging to the script. If the VC asks a question and you say you'll get to it later, you've just told them that your comfort with the slide order matters more than their curiosity. The best founders can drop the deck entirely and have the conversation from memory.

Avoiding or faking hard questions. VCs ask hard questions on purpose. They want to see how you handle uncertainty and whether you're honest about what you don't know. Owning a gap is always better than bluffing through it.

No clear ask or next steps. Every first meeting should end with a concrete next step. Don't let it fade into "let's stay in touch." Ask directly: "What would you need to see to move to a second meeting?" Then follow up on exactly that.

Talking about your idea and not your customers. VCs are not investing in ideas. They're investing in evidence that real people with real problems are willing to pay for your solution. Ground everything you say in specific customer examples and data.

How to Follow Up After a First VC Meeting

The follow-up is where many founders lose deals that were going well. The window is short and the format matters.

Send a follow-up email within 24 hours. Not a week later when you've had time to "think about what to say." The VC is talking to dozens of founders and your conversation will start to blur within days if you don't reinforce it.

Your follow-up should be short. Three to four short paragraphs, no more. Cover: a brief thank-you that references something specific from the conversation (not a generic "great to meet you"); a one-paragraph recap of the key points you want to stick in their mind; any data or materials they asked for during the meeting; and a clear ask for the next step.

Don't use the follow-up to re-pitch everything you covered. You've already had that conversation. Use it to show you listened, you're organized, and you follow through.

If they asked you to send the full deck, your financial model, or customer references, send exactly what they asked for. Nothing more as an attachment dump; nothing less as an excuse to buy more time.

One underused move: include a brief note on something you learned from the conversation. "Your point about distribution in regulated markets was something I hadn't fully thought through. Here's how we're thinking about it now." This shows you're coachable and that the meeting was a real dialogue, not just a pitch you delivered.

What Happens After the First VC Meeting

The honest answer: most first meetings don't lead anywhere. That's normal. The best investors pass on most deals they see, and their reasons are often structural rather than a judgment on your company.

A VC might love your team but be at the end of their fund's deployment cycle. They might have a portfolio company in a related space that creates a conflict. Their thesis might have shifted since they last updated their website. None of this is feedback on whether your startup is good.

What you should pay attention to: how they communicate after the meeting. A fast, specific follow-up asking for more information is a positive signal. A slow, vague response usually isn't.

If you hear nothing for a week, follow up once with something new and useful. A strong metric that just hit, a customer win, or a piece of market data that's relevant to what you discussed. Don't just re-send the same email.

If they pass, ask for feedback and ask for introductions. A VC who passes but respects your company will often be willing to send you to someone who's a better fit. That referral can carry more weight than a cold outreach.

The first meeting with a VC is a skill. It gets better with practice, and almost every founder's second and third meetings are meaningfully sharper than their first. Don't treat your most important target as your first at-bat.

Frequently Asked Questions

What is the goal of a first meeting with a VC?

The goal of a first meeting with a VC is to secure a second meeting, not to close the investment. The first meeting is a high-level compatibility check where both sides are deciding whether it's worth going deeper. Treat it as a conversation about mutual fit, not a pitch for capital.

Should I send my pitch deck before the first VC meeting?

Yes. Sending a non-confidential version of your deck 2–3 days in advance is one of the most effective things you can do before a first VC meeting. It primes the investor to come prepared with specific questions rather than surface-level ones, which makes the conversation far more productive and signals that you're organized and prepared.

What happens if a VC clearly isn't the right fit for my startup?

If you realize mid-meeting that the fit isn't there, pivot the conversation. Acknowledge it directly, then ask for feedback on your approach or introductions to VCs who are a better match. A VC who passes but thinks well of your startup will often send you to someone more appropriate, and that warm referral is worth more than most cold outreach.

How do you follow up after a first VC meeting?

Follow up within 24 hours with a short email: reference something specific from the conversation, recap the two or three points you want to reinforce, attach any materials they asked for, and propose a clear next step. Keep it concise. The follow-up isn't a second pitch; it's a signal that you're organized, you listened, and you follow through.

What do VCs look for in a first meeting?

VCs evaluate five key areas in a first meeting: Team (why you are the right people to solve this problem), Problem (is the pain real and expensive), Solution (what's your product vision and path), Market (is the opportunity large enough to justify a venture return), and Traction (what proof do you have that the market wants what you're building). Of these, team tends to carry the most weight at the pre-seed and seed stage.