Latest Update:

Growth Manager

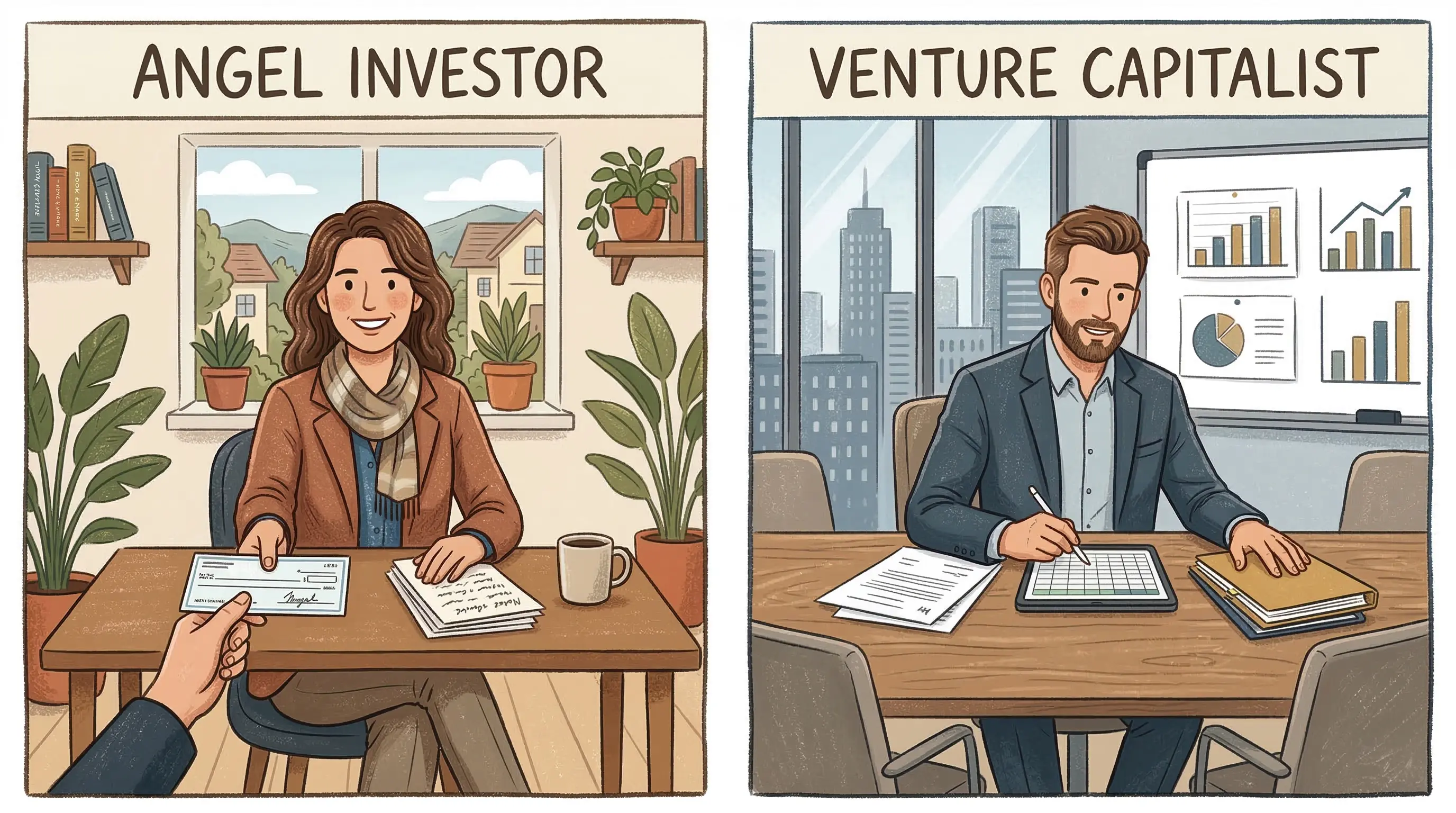

You've got a Pitch Deck, a compelling idea, and you're ready to raise. Then someone asks: "Are you going after Angels or VCs?"

You give a confident answer. But later you wonder: did you actually know what you were choosing?

Most early-stage founders treat this as a simple question of "who will give me money." It's not. Choosing the wrong investor type for your stage can cost you equity, control, and in some cases, momentum you can't afford to lose. As of 2026, with venture capital firms moving earlier than ever and angel syndicates writing seven-figure checks, the lines have blurred further. Getting this decision right matters more, not less.

This guide breaks down everything founders need to know about vc vs angel investors, from how each type works to a practical decision framework you can use right now.

Quick Takeaways

Angel investors put in their own money; venture capital firms invest pooled funds from institutional limited partners.

Angel checks typically range from $25,000 to $500,000; VC investments typically start at $1 million and can reach $100 million or more.

Angels move faster, require less formal due diligence, and take smaller equity stakes (5-25% vs. 20-50% for VCs).

VCs almost always want board seats or observer rights; angels often prefer a passive role.

You can have both on your cap table, and strong angel backers often serve as social proof that accelerates VC interest.

The best investor type depends on your stage, how much you need, and how much operational involvement you want.

What Is the Difference Between a VC and an Angel Investor?

The core difference between a VC and an Angel Investor comes down to whose money is being invested and at what stage. Angel investors invest their own personal funds, typically in early-stage or pre-revenue startups, in exchange for equity. Venture capital firms pool money from institutional investors (pension funds, endowments, family offices) and deploy it into companies with demonstrated growth potential, usually at Series A and beyond.

Here's how they compare across the dimensions that matter most to founders:

Attribute | Angel Investors | Venture Capital Firms |

|---|---|---|

Funding source | Personal capital | Pooled institutional funds |

Typical stage | Pre-seed, seed | Seed (larger firms), Series A and beyond |

Check size | $25,000 to $500,000 | $1 million to $100 million+ |

Equity stake | 5% to 25% | 20% to 50% |

Due diligence | Light; can close in weeks | Rigorous; can take 3-6 months |

Board involvement | Often passive | Board seat or observer rights typically expected |

Decision speed | Fast; one individual decides | Slow; investment committee approval needed |

Mentorship | Variable; depends on individual | Structured; often includes portfolio resources |

This table is a starting point. The real picture is more nuanced, which is why each type deserves a closer look.

How Angel Investors Work

An angel investor is a high-net-worth individual who writes checks from their personal bank account into early-stage companies they believe in. Some are retired founders. Others are current operators, doctors, lawyers, or executives who want to stay close to innovation. Many have built companies themselves and want to give back while making a return.

The typical angel profile: According to the U.S. Securities and Exchange Commission, most angel investors meet the definition of an accredited investor, which means a net worth of at least $1 million (excluding primary residence) or annual income of $200,000 or more for individuals. This threshold isn't a legal requirement for every angel deal, but it's the standard most serious founders use to vet potential investors.

Angel investments tend to cluster between $25,000 and $100,000 for individual checks, though experienced angels with larger portfolios can write $250,000 to $500,000 checks on their own. According to data cited by Business.com, the average angel investment sits around $600,000, which often reflects syndicated rounds where multiple angels pool together.

The Accredited Investor Requirement

Not every wealthy person qualifies as an accredited investor, and not every angel deal requires it. But if you're raising under Regulation D, understanding who can legally invest matters. The SEC's accredited investor definition covers individuals with a net worth over $1 million (excluding their home), income over $200,000 per year (or $300,000 combined with a spouse), or holders of certain professional certifications.

This matters for founders because it shapes who you can pitch without triggering securities registration requirements.

What Angels Bring Beyond the Check

Here's what most articles miss: the check is often the least valuable thing an angel brings.

Strong angels come with industry networks, direct introductions to customers, and something founders almost never talk about: social proof to future VCs. When a well-known operator or former founder backs your pre-seed round, it signals to institutional investors that someone credible has already done diligence on you. It de-risks the story before a VC ever sees your pitch.

Bo Ren, Managing Director of Early-Stage Startups at Silicon Valley Bank, puts it this way: angels are often a combination of operators, scouts, and investors, which means founders get significantly more than capital out of the relationship.

Pro Tip: When evaluating angels, ask yourself: does this person have genuine access to the customers, partners, or investors I'll need in the next 18 months? A $50,000 check from the right person can open doors a $500,000 check from the wrong person never will.

How Venture Capital Firms Work

A venture capital firm is an institutional investor structured as a limited partnership. The firm's general partners (the team managing deals) invest funds raised from limited partners: pension funds, university endowments, sovereign wealth funds, large family offices, and high-net-worth individuals.

The LP/GP structure matters to founders because it explains why VCs behave the way they do. General partners have a fiduciary responsibility to their limited partners. They're managing other people's money. That means every investment decision goes through a process: sourcing, initial screening, partner meetings, due diligence, investment committee approval, and term sheet negotiation. The average Series A deal can take three to six months to close.

[IMAGE: Diagram showing the LP/GP structure of a venture capital firm, with arrows showing money flowing from LPs to the fund, and from the fund to portfolio startups]

The average VC investment is approximately $7 million, according to Marquee Equity, though early-stage funds (often called pre-seed or seed funds) can write checks as small as $500,000. At Series A and beyond, check sizes typically range from $5 million to $15 million, with larger rounds at Series B and C.

In exchange for that capital, VCs typically take 20% to 50% equity and expect operational involvement. Most require at least an observer seat on your board. Many require a full director seat. That's not unreasonable given the size of their commitment, but it's a real shift in how you run your company.

The VC Investment Thesis

Understanding why VCs need outsized returns changes how you pitch them.

A typical venture fund operates on a 10-year horizon and expects that most of its investments will fail or return only modest multiples. The economics only work if one or two portfolio companies return the entire fund. That means VCs aren't looking for good businesses. They're looking for businesses with the potential to be massive.

If your company can realistically grow to $50 million in revenue but probably not to $500 million, a VC fund may genuinely not be the right fit, not because your business isn't good, but because it doesn't match their return requirements.

VC vs Angel Investors: Side-by-Side Comparison

The table above gives you the quick version. Here's the fuller picture across the dimensions founders care most about:

Speed: Angel deals can close in two to four weeks when there's strong conviction. VC processes are structured, with multiple internal gates. Founders who need capital fast, or who are in a hot round, often find angels more responsive.

Dilution: Angels typically take smaller equity stakes than VCs. An angel might take 5-15% for a $200,000 check; a VC might take 25-35% for a $3 million check. Over multiple rounds, the compounding effect of early dilution matters. Getting your first institutional term sheet at a higher valuation (which angels can help you achieve) protects your ownership.

Control: VCs almost always want some form of governance rights. That means board involvement, information rights, pro-rata rights, and sometimes protective provisions that give them veto power over major decisions. Angels are generally content with equity and updates. If maintaining operational control is a priority for you right now, angels give you more of it.

Network value: Both can offer connections, but the type differs. Angels tend to offer warm introductions to customers, early hires, and other angels. VCs tend to offer introductions to later-stage investors, enterprise partners, and talent through portfolio resources. Neither is universally better; it depends on what you actually need next.

Accountability: VC-backed founders operate under more formal reporting expectations. Quarterly updates, board meetings, and metrics reviews become part of the rhythm. Some founders find this discipline helpful. Others find it constraining. Honest self-assessment matters here.

Can You Have Both Angel Investors and VCs?

Yes. And for many startups, this is the natural progression.

The typical path looks like this: angels fund the pre-seed and seed round, the founder builds traction, and that traction (combined with the credibility of named angel backers) makes the Series A conversation easier with institutional investors.

Angels as VC social proof: This is one of the most underappreciated dynamics in early-stage fundraising. When you show up to a VC meeting with a cap table that includes well-known operators, former founders, or recognizable names from a relevant industry, it signals that smart people with real skin in the game already believe in you. It doesn't guarantee a yes, but it changes the starting position of the conversation.

Syndicate angels as a middle ground: Not all angel money comes from individuals writing solo checks. Angel syndicates, groups of angels who pool capital through platforms or informal networks, can write checks in the $250,000 to $2 million range while still offering the speed and flexibility of individual angel investment. For founders who need more than a typical angel round but aren't ready for VC diligence, syndicates can be a real option.

Cap table cleanliness matters: If you take angel money, keep the cap table tidy. VCs are wary of rounds with too many individual investors, each carrying their own pro-rata rights and information requests. Consolidating angels through a Special Purpose Vehicle (SPV) before a Series A is a common way to manage this.

Pro Tip: Before closing your angel round, ask each investor whether they'd participate in a future SPV or convert to a single vehicle if requested by a future VC. Their answer tells you a lot about how founder-friendly they'll be downstream.

Which Is Right for Your Startup? A 5-Question Framework

Most guides tell you "it depends on your stage." That's true but not particularly useful. Here's a more actionable framework. Answer these five questions honestly.

1. How much money do you actually need right now? If you need less than $500,000, angels are almost certainly the right path. VCs have minimum thresholds; deploying $200,000 from a $50 million fund doesn't move their needle. If you need $2 million or more, a VC conversation becomes appropriate, though seed funds may still be the right fit.

2. Do you have product-market fit? VCs want to see demonstrated demand: revenue, strong retention, or clear evidence that your product solves a real problem at scale. If you're still testing assumptions, angel capital gives you the runway to figure it out without the pressure of institutional expectations attached to it. As SVB's Bo Ren notes, taking VC money before finding product-market fit can put you under pressure to make something work without the fundamentals to support it.

3. How much operational involvement do you want from investors? Be honest with yourself here. Some founders genuinely benefit from a board member who pushes them. Others find governance distracting at early stages. Angels are typically more passive. If you want strategic guidance without governance obligations, angel investors fit better.

4. How fast do you need to move? If you have a closing window, a competitive market, or a deal that needs to move quickly, angels win on speed. VC processes are thorough by design.

5. What do you need beyond money? If you need introductions to enterprise customers and downstream institutional investors, a VC's portfolio network might be worth the dilution and governance trade-off. If you need domain expertise, warm referrals to early customers, and credibility signals for your next round, targeted angels with relevant backgrounds will serve you better.

Common Mistakes Founders Make When Choosing Between Angels and VCs

Optimizing for check size instead of fit. A larger check from a misaligned investor is worse than a smaller check from someone who genuinely believes in your vision and has relevant experience. Founders who chase the biggest number often end up with investors who don't understand their market, aren't useful as references, and become difficult cap table members later.

Raising VC money before you're ready. Taking institutional capital before product-market fit is a real risk. You gain runway but lose flexibility. The clock starts ticking on expectations the moment a VC wires money.

Ignoring angels because you think they're "just the first step." The best angels are not just a bridge to VCs. Some of the most valuable investor relationships founders maintain throughout their company's life are angels from the earliest rounds. Don't treat them as placeholders.

Skipping due diligence on your investors. Both angels and VCs deserve scrutiny. Talk to other founders they've backed. Ask about their behavior when things went badly. Reference checks on investors are just as legitimate as investor reference checks on you.

The Fundraising Landscape Has Changed

The vc vs angel investor debate looked different five years ago. Today, many early-stage VC funds have moved significantly earlier, writing $250,000 to $1 million checks into pre-revenue companies. Rolling funds, syndicates, and micro-VCs have created options that didn't exist before. The line between a well-organized angel and a small institutional fund has blurred considerably.

What hasn't changed is the underlying logic. Angels bet on founders. VCs bet on market size and return potential, with founders as a key variable. Understanding which bet you're asking someone to make tells you a lot about which door to knock on first.

Frequently Asked Questions

What is the main difference between angel investors and venture capitalists?

The primary difference is the source of funds and the stage of investment. Angel investors use their own personal capital, typically invest $25,000 to $500,000 in pre-seed or seed-stage startups, and often prefer a passive role. Venture capitalists manage pooled funds from institutional investors, write much larger checks starting at $1 million, and typically require board involvement and governance rights.

Which is better for early-stage startups: angel investors or VCs?

For most early-stage startups (pre-seed to seed), angel investors are the better starting point. They move faster, require less traction, take smaller equity stakes, and impose fewer governance requirements. Venture capital becomes more appropriate once a startup has demonstrated product-market fit and needs significant capital to scale operations.

Do angel investors get equity in return for their investment?

Yes. Angel investors receive equity in exchange for their capital, not loans or revenue-based repayment. The equity percentage depends on the company's valuation at the time of investment and the size of the check. Typical angel equity stakes range from 5% to 25%, though individual deals vary widely.

Can a startup have both angel investors and VCs on its cap table?

Yes, and this is the standard path for many venture-backed startups. Angels typically fund the earliest rounds, and their presence on the cap table, particularly if they are well-known operators or founders, can serve as a positive signal to institutional investors during later fundraising. Many founders consolidate angel investors into a Special Purpose Vehicle before a Series A to keep the cap table manageable.

What do venture capitalists look for before investing?

VCs look for evidence that a startup can achieve massive scale, typically at least $100 million in revenue potential. Key signals include product-market fit, strong retention metrics, a large addressable market, a capable founding team, and a defensible competitive position. Most VC firms also expect some proven traction (revenue, active users, or signed LOIs) before committing capital at the Series A stage.