Latest Update:

Growth Manager

Mailchimp's founders ran their email marketing tool for over a decade serving 13 million users and generating $800 million in annual revenue before Intuit acquired it for $12 billion in 2021. They never gave up a single percentage point of ownership until that exit.

That's not luck. That's a startup booted fundraising strategy working exactly as designed.

A startup booted fundraising strategy is a founder-led approach to raising capital that prioritizes early revenue and customer validation over venture capital dependency. Instead of pitching investors before proving demand, you build traction first and bring in external capital only when it accelerates something that's already working. This guide breaks down exactly how to execute that strategy in 2026: from validating demand before you write a line of code, to building the unit economics that attract investors on your terms.

The conventional wisdom says you raise a seed round, hire fast, burn capital to acquire customers, and repeat every 18 months. But in 2026, with VC selectivity at historic highs and the top 10 venture firms capturing 42.9% of all capital deployed, that path is narrowing fast for founders outside the AI mega-deal environment.

The booted approach gives you a different answer to the question every founder eventually faces: how do you build a company that actually funds itself?

Quick Takeaways

A startup booted fundraising strategy prioritizes revenue, customer validation, and cost discipline over early equity rounds.

It sits between pure bootstrapping and the typical VC path: you maintain control and fund growth through revenue, but stay open to strategic capital when your metrics justify it.

Pre-selling, or collecting payment before the product is fully built, is one of the most underused cash-flow tools in the booted founder's toolkit.

Founders who bootstrap first raise on better terms later because they negotiate from a position of traction rather than desperation.

Non-dilutive funding options including revenue-based financing and government grants can extend runway without giving up equity.

The key metrics to track are MRR, CAC, LTV, and gross margin, not vanity metrics like user counts.

Specific thresholds signal when it's time to transition from a booted approach to external capital.

What Is a Startup Booted Fundraising Strategy?

A startup booted fundraising strategy is a founder-led approach to building a company using internal resources, early revenue, and selective capital, rather than relying on venture capital from the start. Instead of pitching investors before proving demand, founders build traction first and raise externally only when capital accelerates something that's already working.

This is not the same as pure bootstrapping, where a founder refuses outside money entirely. It sits between traditional bootstrapping and the typical VC path: you maintain control and fund growth through revenue, but you stay open to strategic capital when your metrics justify it and your terms are favorable.

Think of it as controlled growth, funded by the business itself, until you have the position to choose your investors rather than chase them.

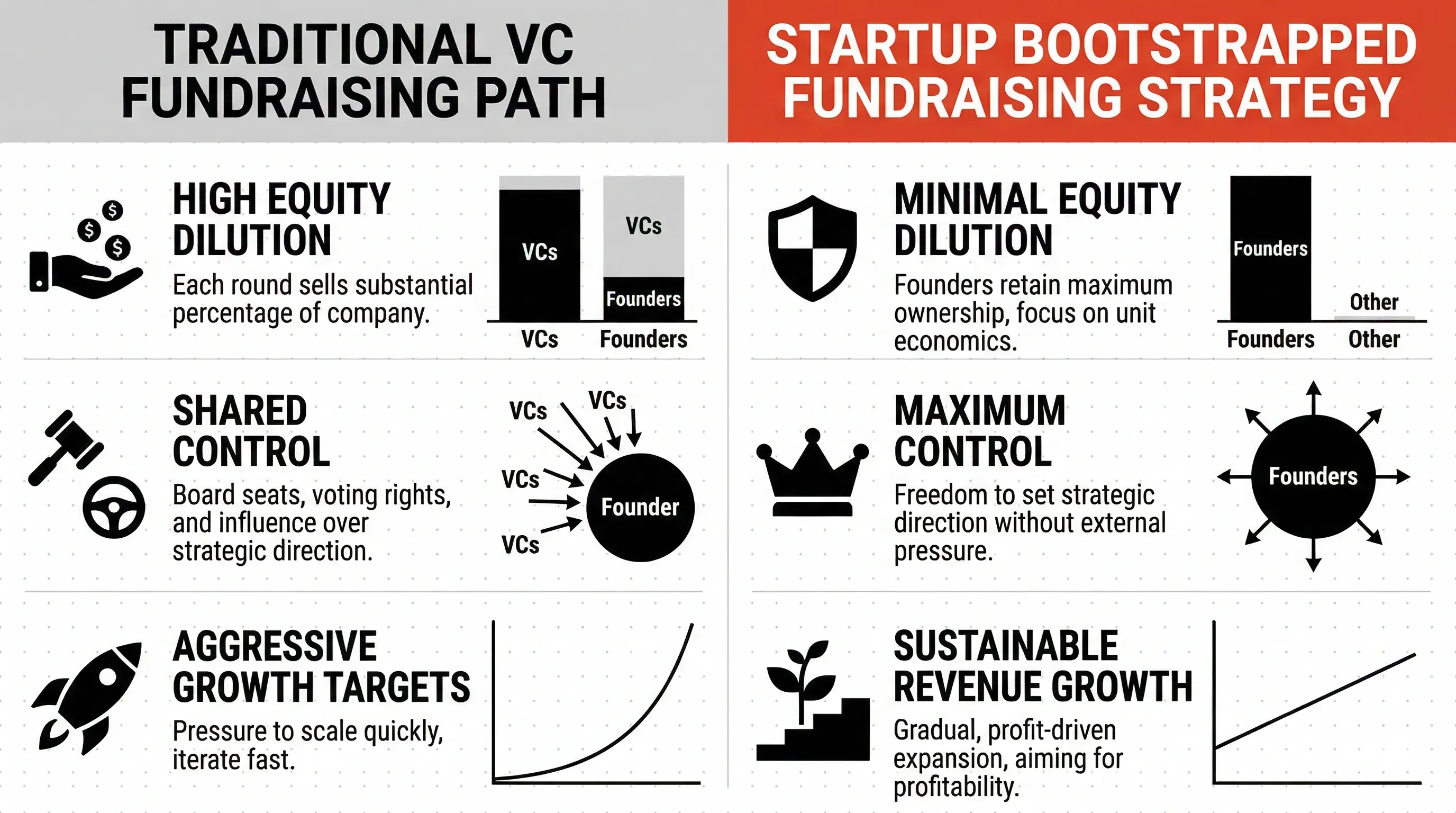

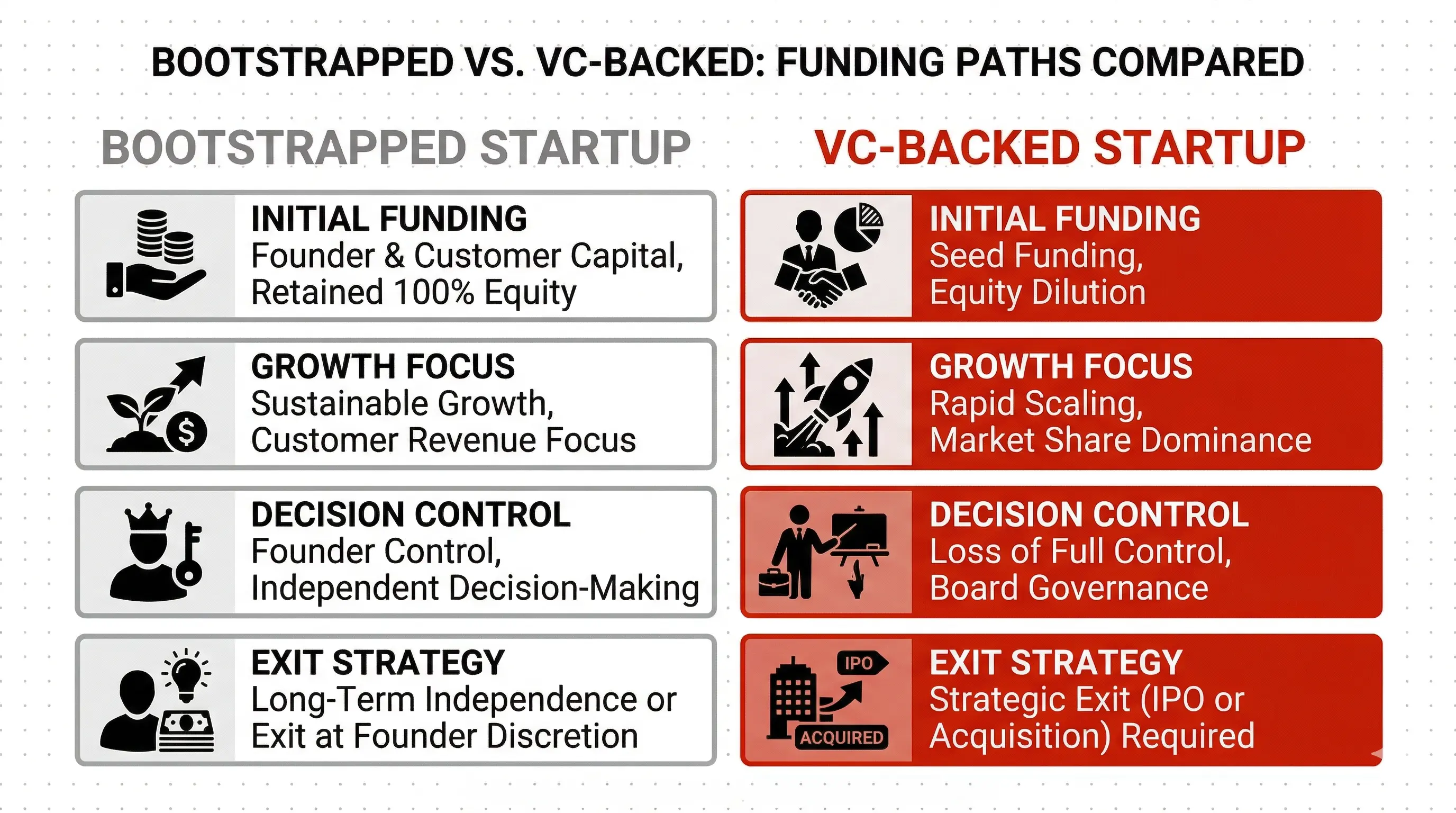

Startup Booted vs. Traditional VC: What's the Actual Difference?

When founders are deciding how to raise capital, two approaches dominate the conversation: bootstrapping (or booted fundraising) and venture-backed funding. Each affects how a company grows and who controls it in fundamentally different ways.

Factor | Startup Booted | Traditional VC |

|---|---|---|

Control | Full founder control throughout | Investor influence from day one |

Capital available | Revenue + selective non-dilutive sources | Large external checks |

Growth speed | Steady, organic, sustainable | Rapid, fueled by capital burns |

Equity dilution | Minimal until you choose to raise | Early and repeated dilution |

Fundraising leverage | Negotiate from traction | Negotiate from pitch |

Investor dependency | Low | High |

Best for | Capital-light models, SaaS, services | Deep tech, hardware, regulated industries |

The booted approach doesn't mean refusing VC forever. It means earning the right to raise capital on your terms. Founders like Jason Fried at Basecamp and the Mailchimp team built businesses with significant revenue before they ever had to consider the terms an investor might demand.

Pro Tip: The single biggest advantage a booted approach gives you isn't cash. It's negotiating position. A founder with $50K MRR and 90% gross margins walks into a fundraise at a completely different table than a founder with zero revenue and a deck.

When a Startup Booted Fundraising Strategy Makes Sense

This strategy isn't right for every startup. It's most effective when specific conditions are true.

When it works well:

Your startup has predictable customer revenue, so you can fund growth from operating cash flow rather than investor checks.

You want to maintain founder control and long-term ownership, and you're building in a space where speed isn't a life-or-death competitive factor.

Your business doesn't require massive capital before product-market fit. SaaS, productized services, and content-led businesses are natural fits.

You want to strengthen your narrative before seeking external capital. Proving traction before approaching investors means you approach them with data, not hypotheses.

You're building a business where the eventual exit or outcome doesn't require a VC's network to materialize.

When it's the wrong call:

You're in a capital-intensive market: hardware, pharmaceuticals, biotech, or deep infrastructure where significant investment is required before any revenue is possible.

Your market has a short window. If being second to market means being irrelevant (think social networks, winner-take-all platforms), raising fast may be the correct strategic move.

You genuinely need investor network access to reach customers or distribution partners you can't reach independently.

The honest answer is that most software and service businesses can execute a booted strategy. Most hardware and regulated businesses can't.

Why More Founders Are Choosing This Path in 2026

The funding environment has shifted. Valuations reset sharply after 2022, VC deal counts declined across most non-AI sectors through 2025, and investors are now demanding stronger traction before writing early-stage checks. Many founders who raised pre-revenue seed rounds five years ago would struggle to close the same deals today.

At the same time, the cost of building a startup has dropped. AI tools, no-code platforms, and remote-first operations mean smaller teams can accomplish more with less upfront capital. The structural conditions that made "raise first, build later" the default playbook have changed.

Founders choosing a startup booted fundraising strategy in 2026 are responding to both sides of this: more selective investors and lower capital requirements. The result is a growing cohort of companies that are further along, more profitable, and less diluted when they eventually do raise.

How to Execute a Startup Booted Fundraising Strategy (Step by Step)

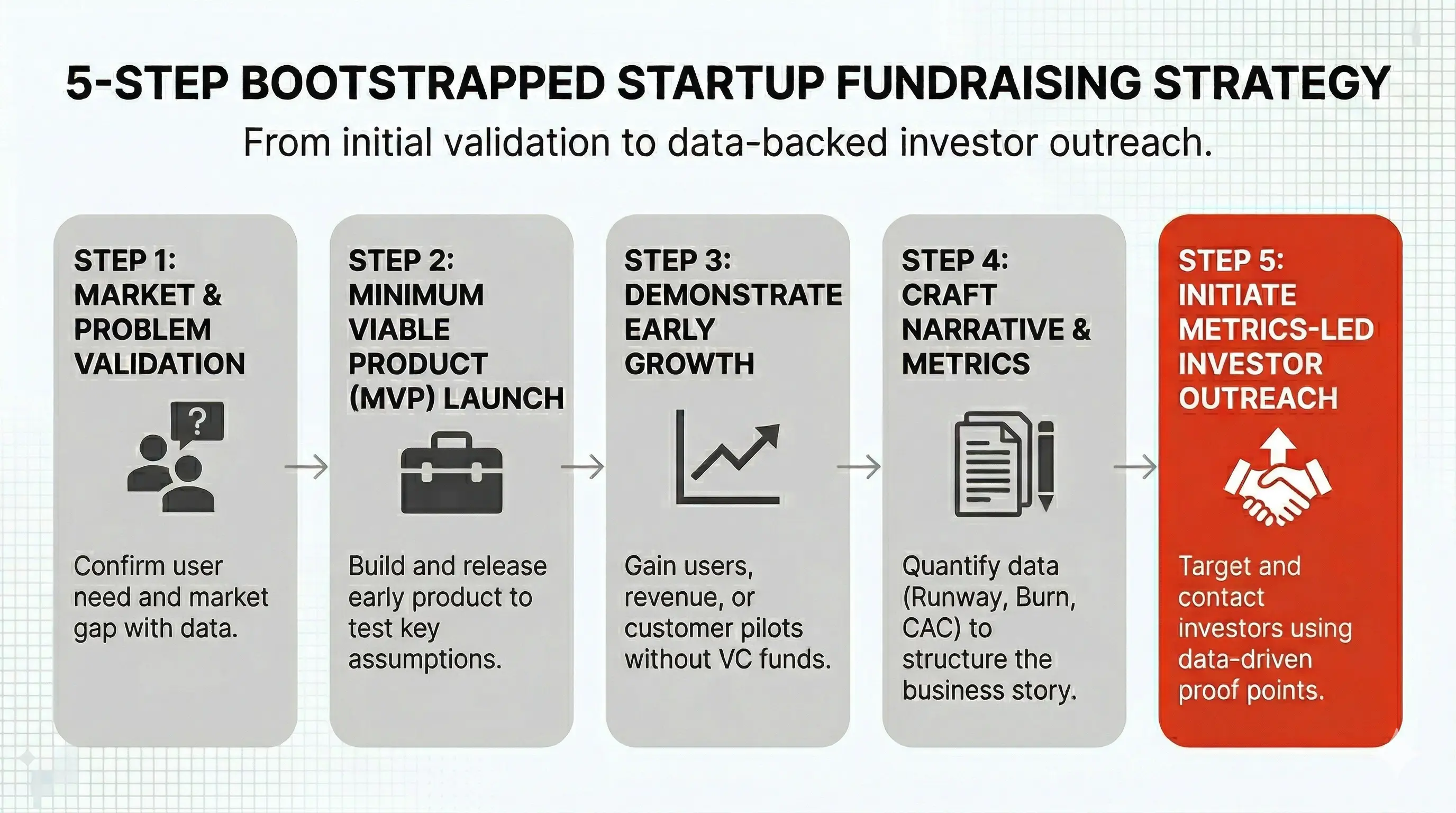

A solid startup booted fundraising strategy follows five stages. Each one builds the proof you need to either sustain yourself through revenue or approach investors on your own terms.

Step 1: Validate Demand Before Writing a Line of Code

Start with the problem, not the solution. Talk to 20 to 30 potential customers before building anything. You're looking for one signal above all others: will people pay for a solution to this problem?

Surveys don't give you this. Conversations do. Ask potential customers to describe the last time the problem cost them money or time. Ask what they're currently using to solve it. Ask what a solution would be worth per month. If you can't get 20 people to have this conversation with you, that's already a signal worth paying attention to.

Step 2: Pre-Sell to Generate Cash Before Launch

Pre-selling is one of the most underused tools in a booted fundraising strategy. The mechanics are straightforward: you offer early access at a discounted rate and collect payment before the product is live.

Done right, this serves three purposes simultaneously. It validates demand with real money rather than intent. It generates cash flow that funds your development sprint. And it gives you a set of early customers who are invested in seeing you succeed and motivated to give you feedback.

Basecamp (formerly 37signals) iterated early products this way. Dozens of successful SaaS companies have funded their first development cycles through pre-sales of $500 to $5,000 per seat. The key is to be specific about what you're promising and when, and to only offer pre-sales to customers whose pain you've already validated in conversations.

Step 3: Launch Lean and Monetize Early

Your minimum viable product (MVP) should do one thing well enough that someone will pay for it. Ship that version fast and charge from day one.

This is where many founders hesitate. They want to add more features before going live, or they worry that charging early will limit growth. The evidence runs the other way. Early monetization forces you to build what customers actually value. Free tiers attract users who have no urgency to get value from your product. Paid customers have skin in the game.

Start with a simple, transparent pricing model. One or two tiers, clear outcomes, no long-term contracts required. You can add complexity later when you understand how customers use the product.

Step 4: Extend Runway Through Cost Discipline

Cost discipline in a booted model is not about being cheap. It's about being intentional. Every dollar you spend should map to either revenue generation or customer retention.

In practice, this means delaying non-essential hires, using contractors for specialized work before you know you have sustained need, and auditing your tool stack for subscriptions that no longer earn their place. Founders who've scaled booted companies consistently report the same pattern: the tightest constraint periods produced their clearest strategic thinking.

Pro Tip: Build a weekly cadence of reviewing your burn against your revenue trajectory. Not monthly. Weekly. It keeps decision-making tight and prevents the slow creep of overhead that kills bootstrapped companies.

Step 5: Build Metrics That Attract Investors on Your Terms

The metrics you track determine the story you can tell when you decide to raise. Booted founders who eventually raise external capital are most compelling when they show clear unit economics, not just growth.

The five metrics that matter most are covered in detail in the section below.

The Metrics That Define a Booted Startup's Fundraising Leverage

When you approach investors after executing a startup booted fundraising strategy, the conversation is completely different from a pre-revenue pitch. You're presenting evidence, not a hypothesis. The table below shows the key metrics, what they signal, and the thresholds that tend to generate investor interest across seed to Series A.

Metric | What It Signals | Healthy Threshold |

|---|---|---|

Monthly Recurring Revenue (MRR) | Predictable revenue base | $20K+ MRR for seed; $100K+ for Series A |

MRR Growth Rate | Momentum | 10-20% month-over-month |

CAC:LTV Ratio | Unit economics | LTV should be 3x CAC or higher |

Gross Margin | Business model quality | 60%+ for SaaS; 40%+ for services |

Net Revenue Retention | Expansion and churn | 100%+ means existing customers are growing spend |

Runway | Financial stability | 12-18 months minimum before raising |

Investors evaluate booted startups differently from pre-revenue deals. They're not betting on a hypothesis. They're pricing a proven model. That shift in framing is what the startup booted fundraising strategy is designed to create.

Risks of a Startup Booted Fundraising Strategy

The booted approach offers real advantages, but it also carries risks founders should understand before committing to the path.

Limited capital availability. Booted fundraising typically relies on revenue and selective funding rather than large investments, which means you may not have enough cash on hand to scale quickly or compete with well-funded rivals. This can slow hiring, limit marketing investment, and create asymmetry against VC-backed competitors.

Slower scalability. Because booted strategies emphasize sustainability and revenue-based growth, you'll often grow more steadily rather than rapidly. In winner-take-all markets where speed is the primary competitive weapon, this is a genuine strategic disadvantage.

Higher personal financial risk. When your company leans on internal revenue and founder resources, it faces financial strain during market downturns or unexpectedly slow periods, especially if runway is thin.

Competitive pressure from VC-backed companies. Rivals with external funding can invest heavily in customer acquisition, product development, and talent before their business model is proven. Executing a booted strategy doesn't eliminate competitive risk; it changes how you manage it.

Understanding these risks doesn't mean avoiding the booted path. It means going into it with clear eyes and a plan for each scenario.

Non-Dilutive Funding Options Bootstrapped Founders Often Overlook

Bootstrapping doesn't mean turning down all external capital. It means being selective about the type of capital you take and when you take it. Several non-dilutive options can extend your runway without requiring equity.

Revenue-Based Financing (RBF) allows startups to borrow against future revenue. Providers like Lighter Capital, Capchase, and Pipe advance capital in exchange for a percentage of monthly revenue until a fixed repayment cap (typically 1.3x to 1.5x the funded amount) is reached. Unlike a traditional loan, payments flex with your revenue. This makes RBF well-suited for SaaS companies with predictable MRR who need capital to accelerate growth without dilution.

SBIR and STTR Programs are U.S. government grants for technology-focused startups. The programs expired on September 30, 2025, and were in a reauthorization lapse for nearly six months. As of March 17, 2026, the House passed S. 3971 (the Small Business Innovation and Economic Security Act) with a 345-41 vote, following unanimous Senate passage on March 3. The bill extends SBIR and STTR authority through September 30, 2031 and is awaiting presidential signature as of late March 2026. Once signed, agencies including the NSF, NIH, and DoD will be able to resume new solicitations and awards. Historically, Phase I grants have ranged from $50,000 to $275,000, and Phase II grants from $750,000 to $1.8 million. If you're building in deep tech, life sciences, defense, or clean energy, monitor sbir.gov closely for the reopening of solicitations.

State and Local Innovation Grants vary by region but many offer $10,000 to $150,000 in non-dilutive funding for early-stage companies meeting local economic development criteria. Check your state's economic development authority.

Strategic Accelerator Programs exist that offer non-dilutive stipends rather than equity stakes. These are less common but worth researching in your industry vertical, particularly in climate tech, health tech, and defense-adjacent sectors.

Customer Prepayments and Annual Contracts are often underused. Offering a 20% discount for annual upfront payment is a legitimate financing mechanism. If you have 10 customers each paying $500/month, converting them to annual contracts at a discount generates $48,000 in immediate cash. That's capital with no dilution and no repayment terms.

Pro Tip: Non-dilutive capital is often invisible to founders who don't actively seek it. Build a tracker: list every grant, RBF provider, and accelerator relevant to your vertical. Revisit it quarterly. One well-timed grant can add 3-6 months of runway at zero dilution cost.

Real Examples of the Booted Strategy Working

Understanding the booted fundraising path is easier when you see it in action across different company types.

Mailchimp started as a side project and grew into a multi-billion dollar email platform without venture capital, focusing on customer value and revenue traction for over a decade before Intuit's $12 billion acquisition in 2021. Their story is now the canonical example of what patient, revenue-first growth produces.

Zoho has remained profitable and privately owned since inception, building a global user base of over 100 million users across its software suite without outside investors. Their approach proves the booted model isn't limited to small companies.

Basecamp bootstrapped growth by prioritizing simplicity and customer trust, deliberately avoiding traditional VC funding. Founder Jason Fried has written extensively about the strategic clarity that comes from not having investor pressure distorting your roadmap.

Shopify is often cited as a VC-success story, but the less-told part of their history is that founder Tobias Lutke bootstrapped and focused on solving a real merchant need for years before choosing to raise capital after demonstrating clear market traction. The traction came first. The capital followed.

These aren't outliers. They're examples of a pattern: the booted approach produces companies with stronger unit economics, clearer product focus, and more negotiating power when capital is eventually sought.

When to Transition from Booted to External Capital

Knowing when to shift from a booted strategy to external fundraising is as important as knowing how to execute the booted phase itself. The signal isn't time-based. It's metrics-based.

Consider raising external capital when:

You have a clear use for capital that will accelerate something already proven to work, not something you're still validating.

Your MRR has reached $20K or above with consistent month-over-month growth.

Your CAC:LTV ratio is at 1:3 or better, meaning you have unit economics that a larger capital injection could scale profitably.

You've identified a market opportunity that requires faster movement than your current revenue can fund, and the cost of moving slowly is genuinely higher than the cost of dilution.

You can approach investors with evidence rather than projections.

The transition from booted to externally funded isn't a failure of the booted strategy. It's the strategy completing its job: you've built the leverage to raise on your own terms.

The Strategic Advantage You Build Before You Ever Raise

Here's something most bootstrapping guides don't say directly: a startup booted fundraising strategy is not just a way to avoid investors. It's a way to make investors compete for access to you.

Atlassian went public in 2015 at a $5.8 billion valuation. Founders Mike Cannon-Brookes and Scott Farquhar maintained significant ownership stakes because they spent years building a profitable, product-led company before ever entering the traditional fundraising conversation. By the time they raised, they were choosing partners, not accepting terms.

That dynamic is available to any founder who builds traction before they need capital. The startup booted fundraising strategy is what creates it.

The companies that ignore this in 2026 will spend the next few years pitching decks to investors who hold all the cards. The ones who execute it will, at minimum, build resilient businesses. And at best, they'll raise on terms that most early-stage founders never get to see.

The first step is the same either way: get a paying customer.

Frequently Asked Questions

What is a startup booted fundraising strategy?

A startup booted fundraising strategy is a founder-led approach to building a company using internal resources, early revenue, and selective capital rather than relying on venture capital from the start. Instead of pitching investors before proving demand, founders build traction first and raise externally only when capital will accelerate something that's already working. It sits between pure bootstrapping and traditional VC fundraising.

How is startup booted fundraising different from pure bootstrapping?

Pure bootstrapping means refusing all outside capital. A booted fundraising strategy is more flexible: you prioritize revenue and maintain founder control, but you stay open to strategic external capital when your metrics justify it and the terms are favorable. The key difference is intent. Booted founders plan to raise eventually. Pure bootstrappers often don't.

When should a pre-seed founder use a booted fundraising strategy?

A pre seed founder should consider a booted fundraising strategy when their business model can generate early revenue without large upfront investment, when they want to maintain equity and control, and when the market doesn't require moving at VC speed to stay competitive. SaaS, productized services, and content businesses are natural fits. Hardware, biotech, and regulated industries usually aren't.

What metrics matter most in a booted fundraising strategy?

The five metrics that matter most are Monthly Recurring Revenue (MRR), MRR growth rate (aim for 10-20% month-over-month at early stages), CAC:LTV ratio (LTV should be at least 3x CAC), gross margin (60% or higher for SaaS), and net revenue retention (100% or above means your existing customers are expanding, not churning). These are the numbers that shift a fundraising conversation from hypothesis to evidence.

What non-dilutive funding options work for booted startups?

Revenue-based financing from providers like Lighter Capital, Capchase, and Pipe lets you borrow against future recurring revenue without giving up equity. The U.S. SBIR/STTR grant programs (currently awaiting presidential signature for reauthorization through 2031 as of late March 2026) offer Phase I grants historically ranging from $50,000 to $275,000 for tech-focused startups. State and local innovation grants, accelerator stipends, and customer prepayments for annual contracts are also practical options that extend runway with zero equity cost.